Financial hardship can arise gradually or all at once. A medical emergency, job loss, divorce, failed business venture, lawsuit, inflation, or rising interest rates can quickly transform manageable debt into a financial crisis. When minimum payments barely cover interest, creditors begin calling daily, and foreclosure or repossession becomes a real threat, bankruptcy may provide structured legal relief.

Bankruptcy is not designed to punish people. It is a federal legal system created to give individuals and businesses a fresh start while ensuring creditors are treated fairly. Whether you are considering personal bankruptcy to eliminate overwhelming consumer debt or business bankruptcy to restructure or close a company, understanding how the system works is essential.

This in-depth guide explains bankruptcy law, types of filings, detailed U.S. bankruptcy and debt statistics, asset protection rules, credit impact, and when to consult experienced bankruptcy attorneys at a qualified bankruptcy law firm.

U.S. Bankruptcy and Debt Statistics

Understanding national trends helps explain why bankruptcy remains an important financial safety net.

National Bankruptcy Filing Trends

According to the Administrative Office of the U.S. Courts:

https://www.uscourts.gov/statistics-reports/caseload-statistics-data-tables

- Total annual bankruptcy filings in the United States typically range between 400,000 and 500,000 cases in recent years, though filings increase significantly during economic downturns.

- Non-business (consumer) cases account for the vast majority of filings, often more than 90% of total cases.

- Chapter 7 filings consistently represent the largest share of personal bankruptcy cases because they offer faster debt discharge.

- Business bankruptcy filings increase during periods of economic instability, high inflation, supply chain disruption, or rising borrowing costs.

- Historically, bankruptcy filings spike after recessions as households and businesses attempt to recover from financial shocks.

Household Debt in America

According to the Federal Reserve Bank of New York Household Debt and Credit Report:

https://www.newyorkfed.org/microeconomics/hhdc

- Total U.S. household debt has surpassed $17 trillion in recent reporting periods, reaching record levels.

- Mortgage balances represent the largest portion of consumer debt, exceeding $12 trillion.

- Credit card debt has surpassed $1 trillion, reflecting increased reliance on revolving credit.

- Auto loan balances remain above $1.5 trillion, with rising delinquencies in certain income brackets.

- Student loan debt exceeds $1.6 trillion nationwide, though federal relief measures have temporarily affected repayment trends.

- Delinquency rates often rise alongside inflation and increased interest rates, contributing to financial strain.

Medical Debt and Bankruptcy

Research published in academic and medical journals has repeatedly shown that medical expenses contribute significantly to personal bankruptcy filings.

https://pubmed.ncbi.nlm.nih.gov/

- Unexpected hospitalizations can generate tens or hundreds of thousands of dollars in charges.

- Even insured individuals may face high deductibles, co-pays, and uncovered treatments.

- Serious illness often reduces income at the same time medical expenses increase.

- Medical debt is one of the leading causes cited in consumer bankruptcy filings.

Small Business Financial Risk

According to the U.S. Small Business Administration:

https://www.sba.gov/

- Small businesses are particularly vulnerable to cash flow interruptions.

- Limited access to capital increases financial fragility.

- Economic downturns and inflation significantly increase default risk.

- Rising interest rates increase borrowing costs, reducing profitability.

- Industry-specific shocks (retail, hospitality, construction) frequently lead to business bankruptcy filings.

These statistics demonstrate that bankruptcy is not rare. It is a structured legal response to widespread financial pressures affecting households and businesses nationwide.

What Is Bankruptcy?

Bankruptcy is a federal court process that allows individuals and businesses to eliminate or restructure debt under court supervision. Its primary purposes include:

- Providing a legal discharge of eligible debts so individuals can break free from compounding interest and collection harassment.

- Creating a court-supervised repayment structure for debtors with income who need time and protection to catch up.

- Preventing aggressive creditor actions through the automatic stay, which immediately halts most collection efforts.

- Ensuring creditors are paid in a fair and legally prioritized order.

- Preserving economic productivity by allowing financially distressed individuals and businesses to reset and recover.

Every bankruptcy case requires full financial disclosure, including income, assets, debts, and recent transactions. Honesty and transparency are critical.

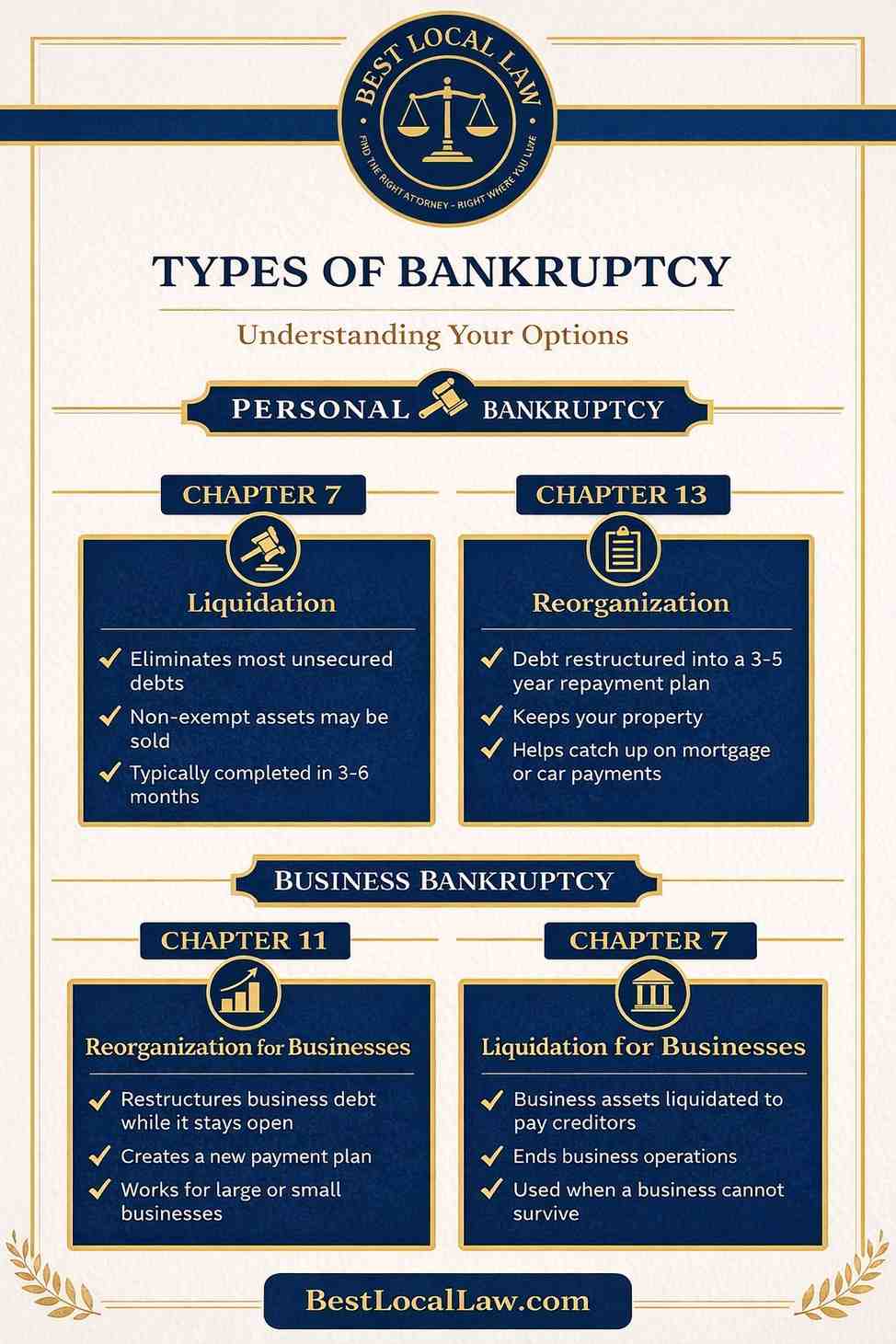

Types of Personal Bankruptcy

Chapter 7 Bankruptcy

Chapter 7, often called a liquidation bankruptcy, is designed for individuals who cannot realistically repay unsecured debts.

Detailed features of Chapter 7 include:

- Filing a petition that lists all assets, liabilities, income sources, monthly expenses, property transfers, and recent financial activity.

- Appointment of a trustee who reviews documentation and determines whether any non-exempt property exists for liquidation.

- Protection of exempt assets under federal or state exemption laws.

- Discharge of most unsecured debts within three to six months.

- Permanent court order prohibiting creditors from attempting further collection on discharged debts.

- Immediate activation of the automatic stay upon filing, halting lawsuits, garnishments, and repossessions.

Common debts discharged under Chapter 7:

- Credit card balances with high interest rates and late penalties that have grown beyond control.

- Medical bills resulting from emergency treatment, surgeries, chronic illness care, or unexpected hospitalization.

- Personal loans from banks, finance companies, or online lenders.

- Utility arrears such as electric, gas, or water bills.

- Certain deficiency balances after foreclosure or repossession.

Debts generally not discharged:

- Child support and alimony obligations.

- Most student loans are discharged unless undue hardship is proven in a separate legal proceeding.

- Recent income taxes and payroll tax liabilities.

- Criminal restitution and court fines.

- Debts obtained through fraud or intentional misconduct.

Advantages of Chapter 7:

- Fast resolution compared to repayment plans.

- No long-term repayment obligation.

- Immediate relief from creditor harassment.

- Opportunity for a true financial reset.

Potential disadvantages:

- Possible liquidation of non-exempt assets.

- Impact on credit report for up to 10 years.

- Strict eligibility through the means test.

A skilled bankruptcy lawyer can evaluate whether Chapter 7 is appropriate and protect as many assets as possible.

Chapter 13 Bankruptcy

Chapter 13 is designed for individuals with regular income who need a structured repayment plan.

Detailed characteristics of Chapter 13 include:

- Creation of a court-approved repayment plan lasting three to five years.

- Consolidation of multiple debts into one monthly trustee payment.

- Opportunity to catch up on mortgage arrears while stopping foreclosure permanently.

- Protection from vehicle repossession if payments are maintained.

- Potential restructuring of certain secured debts.

- Discharge of remaining eligible unsecured debt after successful completion of the plan.

Advantages of Chapter 13:

- Ability to retain non-exempt property.

- Structured and predictable payment schedule.

- Protection against foreclosure when payments are made consistently.

- Opportunity to repay priority debts in manageable installments.

Challenges of Chapter 13:

- Requires stable and sufficient income.

- Long-term financial discipline.

- Risk of dismissal if payments are missed.

Bankruptcy attorneys are essential in designing feasible repayment plans that courts will approve.

Business Bankruptcy Options

Chapter 11 Bankruptcy

Chapter 11 allows businesses to reorganize rather than close.

Key elements include:

- Continued operation of the business during restructuring.

- Development of a reorganization plan outlining debt repayment or modification.

- Renegotiation of contracts, leases, and loan terms.

- Possible sale of underperforming divisions.

- Creditor voting on the proposed plan.

- Court oversight of financial restructuring.

Subchapter V simplifies Chapter 11 for qualifying small businesses by:

- Reducing administrative expenses.

- Shortening confirmation timelines.

- Limiting creditor committee requirements.

- Allowing owners to retain equity under certain conditions.

Chapter 7 Business Liquidation

When continuation is not viable, Chapter 7 allows:

- Orderly liquidation of assets, including equipment, inventory, and real estate.

- Trustee-managed sale of business property.

- Distribution of proceeds to creditors according to priority rules.

- Formal dissolution of the business entity.

Businesses do not receive a discharge; they cease operations.

The Bankruptcy Process

The general steps include:

- Initial consultation with a bankruptcy lawyer to evaluate financial history, income stability, asset protection needs, and goals.

- Completion of mandatory credit counseling from an approved provider.

- Detailed preparation of bankruptcy schedules listing assets, debts, income, expenses, and recent transactions.

- Filing of petition in federal bankruptcy court.

- Immediate activation of the automatic stay.

- Attendance at the 341 Meeting of Creditors, where the trustee verifies information under oath.

- Discharge of debts (Chapter 7) or confirmation of repayment plan (Chapter 13 or 11).

Accuracy is essential. Omissions or errors can result in dismissal of the case or legal penalties.

What Property Can You Keep?

Bankruptcy exemptions protect essential assets. Depending on state law, protected property may include:

- Equity in a primary residence under homestead exemption rules, which vary significantly by state.

- A vehicle necessary for commuting to work, subject to value limits.

- Household furnishings, clothing, appliances, and personal effects up to statutory thresholds.

- Retirement accounts such as 401(k)s, IRAs, and pensions, which are often fully exempt under federal law.

- Tools and equipment necessary for employment or business operations.

- Public benefits, including Social Security, disability payments, and unemployment compensation.

An experienced bankruptcy law firm ensures exemptions are maximized to preserve stability.

How Bankruptcy Affects Credit

Although bankruptcy initially lowers credit scores, many individuals recover faster than those who continue struggling with delinquent accounts.

- Chapter 7 appears for up to 10 years.

- Chapter 13 appears for seven years.

- Many individuals qualify for secured credit cards within months of discharge.

- Responsible credit use after discharge can significantly improve scores over time.

- Mortgage eligibility may return within two to four years, depending on the loan type.

When to Contact Bankruptcy Attorneys

You should consult bankruptcy attorneys if:

- You rely on credit cards to pay for basic living expenses.

- Collection calls and lawsuits are increasing.

- Wage garnishment has begun or is threatened.

- Foreclosure notices have been received.

- Your business cannot meet payroll or tax obligations.

- Debt continues to grow despite consistent payments.

- You are considering withdrawing retirement funds to pay unsecured creditors.

Early consultation often protects more assets and expands available options.

Frequently Asked Questions

- How long does bankruptcy take?

Chapter 7 takes three to six months. Chapter 13 lasts three to five years. - Will I lose my house?

Many homeowners retain their property, particularly under Chapter 13. - Can bankruptcy stop lawsuits?

Yes, the automatic stay halts most legal proceedings. - What debts are non-dischargeable?

Child support, alimony, most student loans, recent taxes, and criminal fines. - Is bankruptcy a public record?

Yes, but it is not broadly publicized. - Can I file more than once?

Yes, but waiting periods apply. - Will my employer find out?

Usually, only if payroll adjustments are required. - Can creditors object?

Yes, but objections are uncommon in standard cases. - How much does a bankruptcy lawyer cost?

Fees vary based on chapter and complexity. - Can business owners eliminate personally guaranteed debts?

Possibly, depending on structure and filing type. - What is the automatic stay?

A court order that stops most collection actions immediately. - Can I keep my car?

Often yes, particularly in Chapter 13 or if payments are current. - Should I use retirement funds instead?

Retirement accounts are often protected, so legal advice is essential before making any withdrawals. - Does bankruptcy clear medical debt?

Yes, medical debt is typically dischargeable. - When should I contact a bankruptcy law firm?

As soon as debt becomes unmanageable, repayment is unrealistic. Early legal guidance improves outcomes.

Final Thoughts

Bankruptcy remains a critical part of the American financial system. With trillions in household debt and hundreds of thousands of filings annually, it provides a structured path toward financial recovery. Whether pursuing personal bankruptcy or business bankruptcy, consulting an experienced bankruptcy lawyer is essential. Skilled bankruptcy attorneys at a reputable bankruptcy law firm can guide you through the legal process, protect your assets, and help you rebuild financial stability with confidence.